By Ruth Thorlby, Assistant Director, Policy, The Health Foundation

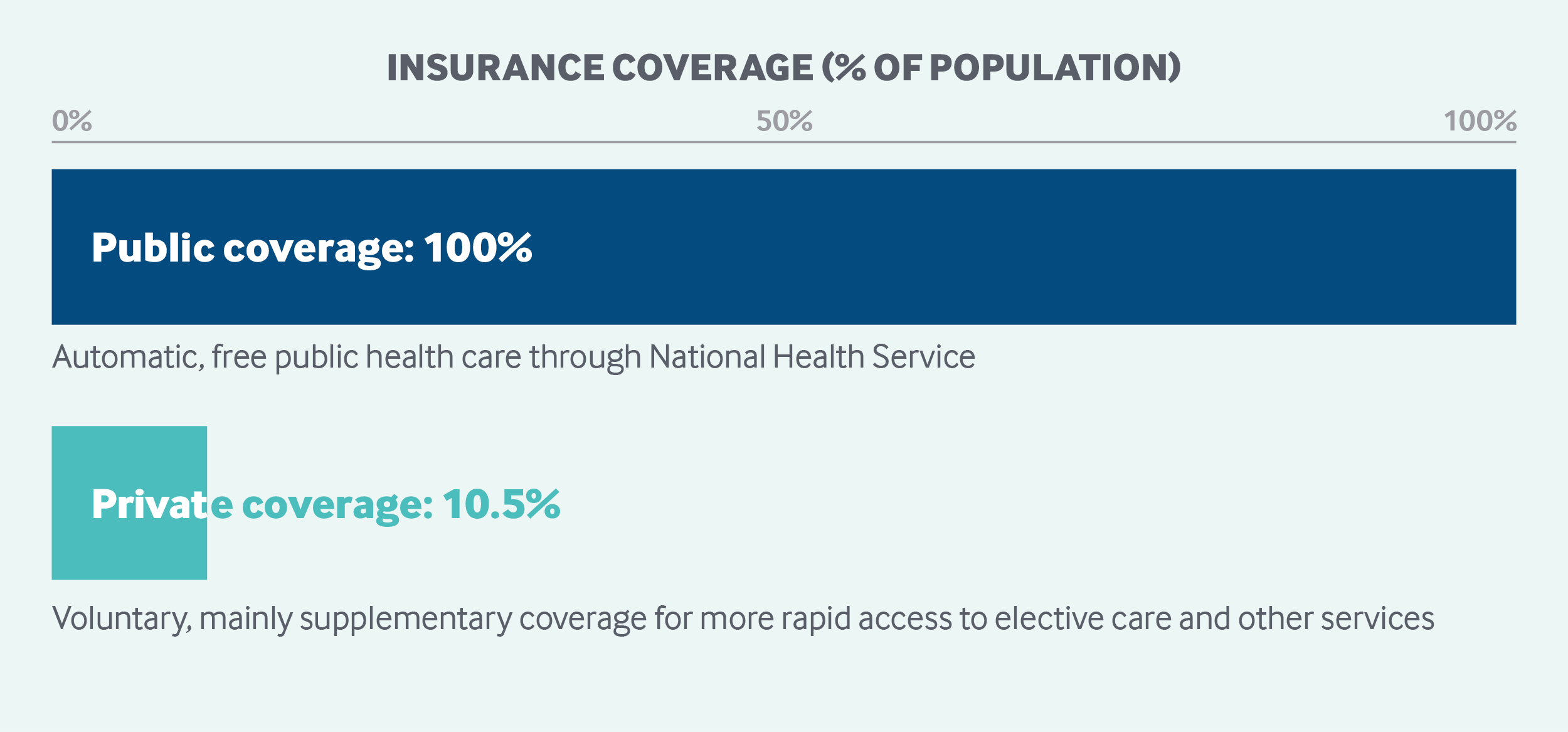

All English residents are automatically entitled to free public health care through the National Health Service, including hospital, physician, and mental health care. The National Health Service budget is funded primarily through general taxation. A government agency, NHS England, oversees and allocates funds to 191 Clinical Commissioning Groups, which govern and pay for care delivery at the local level. Approximately 10.5 percent of the United Kingdom’s population carries voluntary supplemental insurance to gain more rapid access to elective care.1

Sections

How does universal health coverage work?

Health coverage in England has been universal since the creation of the National Health Service (NHS) in 1948. The NHS was set up under the National Health Service Act of 1946, based on the recommendations of a report to Parliament by Sir William Beveridge in 1942. The Beveridge Report outlined free health care as one aspect of wider welfare reform designed to eliminate unemployment, poverty, and illness, and to improve education. Under the 1946 Act, the Minister of Health had a duty to provide a comprehensive, free health service, replacing voluntary insurance and out-of-pocket payments.2

Currently, all those “ordinarily resident” in England are automatically entitled to NHS care, still largely free at the point of use, as are nonresidents with a European Health Insurance Card. For other people, such as non-European visitors or undocumented immigrants, only treatment in an emergency department and for certain infectious diseases is free.3 Rights for those eligible for NHS care are summarized in the NHS Constitution; they include the right to access care without discrimination and within certain time limits for certain categories, such as emergency and planned hospital care.4

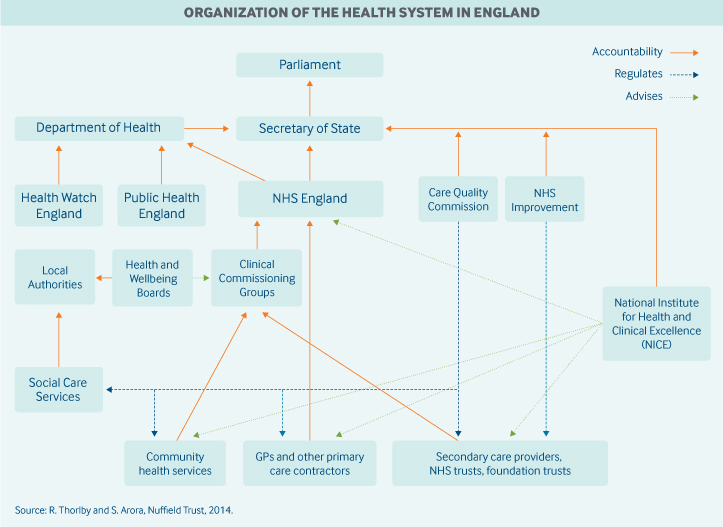

Role of government: Responsibility for health legislation and general policy in England rests with Parliament, the Secretary of State for Health, and the Department of Health. Day-to-day responsibility for the NHS lies with NHS England, an arm’s-length, government-funded body run separately from the Department of Health.5 Its responsibilities include:

- managing the NHS budget

- overseeing 191 local Clinical Commissioning Groups (CCGs), which are groups of local general practitioners (GPs) who plan, commission, and pay for most of the hospital and community care service in their areas

- directly commissioning certain types of care, including primary care in some areas, dental care, treatments for rare conditions, and some public health services (such as immunizations)6

- working toward objectives in the annual mandate from the Secretary of State for Health, which include both efficiency and health goals

- setting the strategic direction of health information technology, including the development of online services to book appointments and the setting of quality standards for electronic medical record-keeping and prescribing.

The government owns the hospitals and providers of NHS care, including ambulance services, mental health services, district nursing, and other community services. These providers are called NHS trusts.

Other important public agencies involved in health care governance include:

- NHS Improvement, which licenses all providers of NHS-funded care and may investigate potential breaches of NHS cooperation and competition rules, as well as mergers involving NHS foundation trusts

- the Care Quality Commission, which ensures basic standards of safety and quality by registering providers and monitoring the achievement of care standards

- the National Institute for Health and Care Excellence, which sets guidelines for clinically effective treatments and appraises new health technologies for their efficacy and cost-effectiveness

- Health Education England, which plans the NHS workforce.

Role of public health insurance: In 2016, the U.K. spent 9.8 percent of GDP on health care; public expenditures, mainly related to the NHS, accounted for 79.4 percent of this amount.7 The majority of NHS funding comes from general taxes, and a smaller proportion (20%) comes from national insurance, which is a payroll tax paid by employees and employers. The NHS also receives income from copayments and people using NHS services as private patients.

Role of private health insurance: In 2015, an estimated 10.5 percent of the U.K. population had private voluntary health insurance, with nearly 4 million policies held at the beginning of 2015.8 In 2016, voluntary private health insurance accounted for 3.3 percent of total health expenditures.9

Some private insurance is offered by employers, but individuals can also purchase policies. Private insurance offers more rapid access to care, choice of specialists, and better amenities, especially for elective hospital procedures; however, most policies exclude mental health, maternity services, emergency care, and general practice.10 According to a 2014 investigation, four insurers account for 87.5 percent of the private insurance market, with small companies making up the rest.11

Services covered: The precise scope of services covered by the NHS is not defined in statute or by legislation, and there is no absolute right for patients to receive a particular treatment. However, the statutory duty of the Secretary for Health is to ensure comprehensive coverage.

In practice, the NHS provides or pays for the following:

- preventive services, including screenings, immunizations, and vaccination programs

- inpatient and outpatient hospital care

- maternity care

- physician services

- inpatient and outpatient drugs

- clinically necessary dental care

- some eye care

- mental health care, including some care for those with learning disabilities

- palliative care

- some long-term care

- rehabilitation, including physiotherapy (such as after-stroke care)

- home visits by community-based nurses

- wheelchairs, hearing aids, and other assistive devices for those assessed as needing them.

The volume and scope of these services are generally a matter for local decision-making by CCGs.

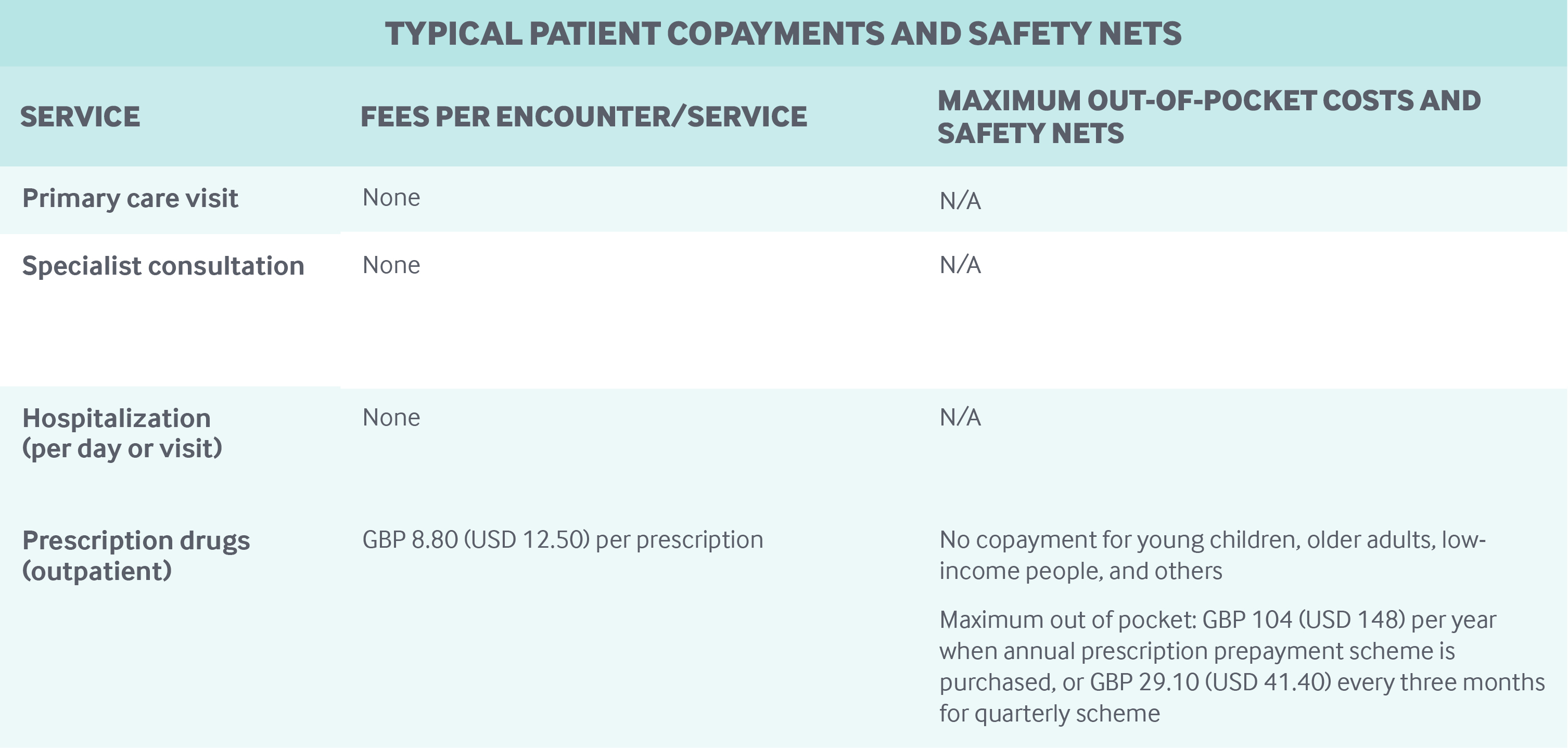

Cost-sharing and out-of-pocket spending: The NHS has very limited cost-sharing arrangements for publicly covered services. Services are free at the point of use for outpatient and inpatient hospital services. Out-of-pocket payments for GP visits apply only to certain services, such as the provision of certificates for insurance purposes and travel vaccinations. NHS screening and vaccination programs are not subject to copayments.

Outpatient prescription drugs are subject to a copayment of GBP 8.80 (USD 12.50) per prescription. Drugs prescribed in NHS hospitals are free.

NHS dentistry services are subject to copayments of up to GBP 256.50 (USD 365.00) per course of treatment.12 These charges are set nationally by the Department of Health.

Out-of-pocket health expenditures by households accounted for 15 percent of total expenditures in the U.K. in 2016. Also in 2016, the largest portion of out-of-pocket spending (37%) was on long-term care services, including residential care, followed by 35 percent for medical goods (including pharmaceuticals).13

Safety nets: In 2016, 89 percent of prescriptions in England were dispensed free of charge.14 People who are exempt from prescription drug copayments include:

- children age 15 and under

- full-time students ages 16 to 18

- people age 60 or older

- people with low incomes

- pregnant women and women who have given birth in the past 12 months

- people with cancer and certain other long-term conditions or disabilities.

Patients who need large amounts of prescription drugs can buy prepayment certificates costing GBP 29.10 (USD 41.40) for three months and GBP 104 (USD 148) for 12 months. Users incur no further charges for the duration of the certificate, regardless of how many prescriptions they need.

Other safety nets include assistance with dental and vision care. Young people, students, pregnant and recently pregnant women, prisoners, and those with low incomes are not liable for dental copayments. Vision tests are free for young people, those over age 60, and people with low incomes. In addition, young people and those with low incomes can obtain financial support to meet the cost of corrective lenses.

Transportation costs to and from provider sites also are covered for people who qualify for the NHS Low Income Scheme.

How is the delivery system organized and how are providers paid?

Physician education and workforce: There is a growing shortage of doctors, affecting primary care and certain specialties. In 2016, the government promised an additional 5,000 GPs by 2021, including new trainees, overseas recruits, and physicians returning to practice.15 Financial incentives have been made available to trainees and returnees to attract doctors to areas where there are shortages, including rural and urban areas.

The government regulates the number of university slots for undergraduate medical and dentist degrees: In 2018–2019, a total of 6,700 places were available for medical degrees across public universities in England.16 This is 500 more slots than were available in 2017–2018. Over time, the government has promised to expand the number of undergraduate training slots by 25 percent to address the workforce shortage.

Undergraduate degrees are financed through student fees and government subsidies. The remainder of medical training (four to six years) is funded by government.

Primary care: Primary care is delivered mainly through GPs, who act as gatekeepers for secondary care. General practices are normally patients’ first point of contact, and people are required to register with a local practice of their choice; however, choice is effectively limited because many practices are full and do not accept new patients. In some areas, walk-in centers offer primary care services, for which registration is not required.

In September 2017, there were approximately 34,000 GPs (full-time equivalents) in nearly 7,400 practices, with an average of about 8,000 patients per practice and 1,400 patients per GP.17 Eleven percent of practices were solo practices in 2017, while 46 percent had five or more GPs.

Most GPs (59.4 percent) are private contractors (self-employed). The proportion of GPs employed in practices or on a salaried basis as locums (standing in when other GPs are unavailable) is increasing and is currently around 22 percent.

Most (69%) of practices operate under General Medical Services contracts, negotiated between the British Medical Association (representing doctors) and government. Physician payment is about 60 percent capitation for essential services, about 15 percent fee-for-service payments for optional additional services (such as vaccines for at-risk populations), and about 10 percent performance-related payments.18 Capitation is adjusted for age and gender, local levels of morbidity and mortality, the number of patients in nursing and residential homes, patient list turnover, and a market-forces factor for staff costs as compared with those of other practices. Performance bonuses are given mainly on evidence-based clinical interventions and care coordination for chronic illnesses.

General practice is undergoing a structural change, from single-handed corner shops to networked practices, including larger organizations using multidisciplinary teams of specialists, pharmacists, and social workers.19 The average income for GPs (contracted and salaried) in England was GBP 92,500 (USD 131,579) before tax in 2015–2016, with GPs earning 82 percent of what specialists earn.20

Most general practices employ other professionals on salaries, such as nurses, whose duties include managing patients with long-term conditions, and providing minor treatments. In December 2017, there were about 15,800 nurses working in general practice.21

Outpatient specialist care: Nearly all specialists are salaried employees of NHS hospitals. Salaries are agreed on as part of a national contract between the Department of Health and the British Medical Association.

As of the end of 2017, there were approximately 45,800 hospital specialists and 52,800 hospital doctors in training.22

CCGs pay hospitals for outpatient consultations at nationally determined rates. Specialists are free to engage in private practice within specially designated wards in NHS or private hospitals. In 2006, an estimated 55 percent of doctors performed private work, a proportion that is declining as the earnings gap between public and private practice narrows.23

Patients are able to choose which hospital to visit, and the government has introduced the right to choose a particular specialist within a hospital. Most outpatient specialist consultations are carried out in hospitals, although a small proportion of consultations take place in general practices.

Administrative mechanisms for direct patient payments to providers: U.K. residents do not pay for physician services, which are all free at the point of use. The bulk of general practices are reimbursed monthly by NHS England for the services they deliver on the basis of data extracted automatically from practices’ electronic records. Some payments may require practices to enter data manually on the number of patients screened or treated for “enhanced services” that qualify for additional payments, such as diagnosis and support for patients with dementia. These data are collated and validated by NHS England.

After-hours care: Since 2004, GPs are no longer required to personally provide after-hours care to their patients; however, GPs must ensure that adequate arrangements for after-hours care are in place. In practice, this means that CCGs contract mainly with GP cooperatives and private companies for after-hours care, both of which usually pay GPs on a per-session basis.

Providers are expected to send electronic discharge summaries to the patient’s usual GP within 24 hours of using an emergency service.

Serious emergencies are handled by hospital emergency departments. In some areas, less-serious cases are seen in urgent care centers or minor-injury units, which are staffed in a variety of ways and include both nurse-led and GP-led centers (paid per session). These are generally NHS-run and can be free-standing or attached to a hospital.

Telephone advice is available on a 24-hour basis through NHS 111 for those with an urgent but not life-threatening condition. Callers are able to speak to a clinician, if appropriate, after triage.

Hospitals: Publicly owned hospitals are organized either as NHS trusts (currently 64) directly accountable to the Department of Health or as foundation trusts (currently 142) regulated by NHS Improvement.24 Foundation trusts have more freedom to borrow and invest and have local people and staff involved in governance.

All public hospitals contract with local CCGs to provide services. They are reimbursed mainly at nationally determined diagnosis-related group (DRG) rates, which include medical staff costs. DRG payments account for about 60 percent of hospital income, with the remainder coming from activities not covered by DRGs, such as mental health, education, and research and training funds.25 For some services, such as community services, payment is made for the overall service. Bundled payments (such as for the total annual cost of care per diabetic patient) are being developed at the local level but are not yet in widespread use. There is no cap on hospital incomes.

Responsibility for setting DRG rates is shared between NHS England and NHS Improvement. Some DRG rates are set to incentivize best practices, such as the use of day-case surgery (same-day surgery) when appropriate.

There are an estimated 515 private hospitals offering health care services in the U.K., a mixture of for-profit and nonprofit.

There are no comprehensive public data on the total number of patients treated in private hospitals, but of the 285 hospitals that submitted data in 2017, 735,522 patients received treatment. By comparison, more than 8.5 million nonurgent patients were treated by the NHS that year.26

Private hospitals offer a range of services, including treatments either unavailable in the NHS or subject to long waiting times, such as bariatric surgery and fertility treatment, but generally do not have emergency, trauma, or intensive-care facilities.27 Private providers must be registered with the Care Quality Commission and with NHS Improvement, but their charges to private patients are not regulated, and there are no public subsidies. Although the volume of care purchased from private providers by the NHS has increased recently in areas outside of mental health, NHS use of private providers remains low: 7.6 percent of overall spending by CCGs on hospital services in 2015–2016.28

Mental health care: Mental health care is an integral part of the NHS and covers a full range of services. Less-serious illnesses — mild depressive and anxiety disorders, for example — are usually treated by GPs. Those requiring more advanced treatment, including inpatient care, are treated by specialist mental health trusts. Some of these services are provided by community-based practitioners. About a quarter of NHS-funded, hospital-based mental health services are provided by the private sector.

Over the past decade, policy has focused on expanding services for mild-to-moderate adult mental health problems, such as depression and anxiety, through the Increasing Access to Psychological Therapies program, which integrates mental health into primary care. In 2017–2018, 550,479 people referred to the program completed courses of therapy, lasting an average of six weeks.29

Long-term care and social supports: The NHS pays for long-term care (at home or in residential facilities) for people with care needs arising from illness, disability, or accident, including at the end of life. About 135,000 people were receiving this form of care at the end of 2018.30

All other long-term services and supports are paid either out of pocket or by local authorities. Local authorities are legally obliged to assess the needs of all people who request these services. Unlike NHS services, however, locally funded social care is not typically free at the point of use, except for certain services (such as time-limited rehabilitation services for people recovering from illnesses or injuries, the provision of some equipment, and home modifications).

To receive regular financial support for home care, nursing care, and residential care, individuals need to pass a needs and a means test. Full local authority support for residential care, for example, is available only to those with high care needs and less than GBP 14,250 (USD 20,270) in assets, with a sliding scale discount applied to assets up to GBP 23,250 (USD 33,072). There is a national framework for assessing need, but local authorities are free to set eligibility thresholds, which have become progressively more restricted over the past decade.31 Local authorities fund long-term care from local taxes and grants from central government. Central government funding for local authorities has fallen an estimated 49 percent in real terms between 2010–2011 and 2017–2018.32

Those who qualify for local authority funding are liable for copayments, with some people contributing almost all of their assessed income, including pensions. Funding can be managed by the local authority (paying providers directly), or people can receive direct payments to purchase their own care, with the supervision of the local authority. In 2016–2017, GBP 15.0 billion (USD 21.3 billion) was spent on locally funded long-term care in England, of which GBP 1.8 billion (USD 2.6 billion) was spend on direct payments. Nearly 870,000 people received services in a nursing home, in a residential home, or at home. Community-based services were the most common: 75 percent of people received services in their home.33

Some additional allowances paid to users and caregivers are exempt from means testing, such as an attendance allowance worth a maximum of GBP 82.30 (USD 117.00) a week. An estimated 8 percent of the U.K. population are informal carers (5.4 million people), 33 percent of whom are caring for a parent outside their own household.34

In 2017, the private sector (for-profit and nonprofit) provided 78 percent of residential care places for older people and the physically disabled in the U.K., and 86 percent of nursing home places.35

The NHS provides end-of-life palliative care at patients’ homes, in hospices (usually run by charitable organizations), in care homes, or in hospitals.

Separate government funding is available for working-age people with disabilities.

What are the major strategies to ensure quality of care?

The Care Quality Commission regulates all health and adult social care in England. All providers, including institutions, individual partnerships, and sole practitioners, must be registered with the commission, which monitors performance using nationally set quality standards and investigates individual providers when concerns are raised by patients and others. It rates hospitals’ inspection results and can close down poorly performing services. The monitoring process includes results of annual national patient experience surveys for hospital, mental health, community, primary care, and ambulance services.

The National Institute for Health and Care Excellence develops quality standards, guidance, and guidelines for a large range of clinical conditions, safe staffing levels, technologies, medicine handling, antimicrobial prescribing, and diagnostics, which span primary, secondary, and social care services. National strategies have been published for a range of conditions, from cancer to trauma. There are national registries for key disease groups and procedures. Maximum waiting times have been set for cancer treatment, elective treatments, and emergency treatment. A website, NHS Evidence, provides professionals and patients with up-to-date clinical guidelines.

Information on the quality of services at the organization, department, and (for some procedures) physician levels is published on the NHS website. Results of inspections by the Care Quality Commission are also publicly accessible.

The Quality and Outcomes Framework provides general practices with financial incentives to improve quality. General practices are awarded points (which determine a portion of their remuneration) for keeping a disease registry of patients with certain diseases or conditions, including data on patient management and treatment. For hospitals, 2.5 percent of contract value is linked to the achievement of a limited number of quality goals through the Commissioning for Quality and Innovation initiative. In addition, DRG rates for some procedures are linked to compliance with best practices.

All doctors are required by law to have a license from the General Medical Council to practice. Similar requirements apply to all professions working in the health sector. A revalidation process every five years has been introduced for doctors, nurses, and midwives.

Healthwatch England promotes patient interests nationally. In each community, local Healthwatches support people who make complaints about services; quality concerns may be reported to Healthwatch England, which can then recommend that the Care Quality Commission act. In addition, local NHS bodies, including general practices, hospital trusts, and CCGs, are expected to support their own patient engagement groups and initiatives.

What is being done to reduce disparities?

The Secretary of State, Public Health England, NHS England, and CCGs have a legal duty to “have regard” for the need to reduce health disparities, although the applicable legislation does not specify what actions need to be taken. NHS England publishes an annual report on the actions taken and progress being made in reducing disparities in access and outcomes, by gender, disability, age, socioeconomic status, and ethnicity.36

NHS strategies include:

- ensuring that local CCG areas receive adequate resources to tackle inequalities

- measuring progress toward reducing disparities

- financially incentivizing reductions in inequalities in certain areas, such as early cancer diagnosis and mental health

- sharing best practices for achieving targeted goals, such as care for homeless people

- using risk stratification tools to identify people at risk of ill health.

Public Health England also has been tasked with reducing health inequalities and has published extensive guidance for local authorities.37 The agency also publishes data on progress in a health equity “dashboard.”38 Budgets for public health are held by local government authorities, which are required to host health and well-being boards to improve coordination of local services and reduce health disparities. Using local taxes and grants from central government, local government also funds social services for children and adults, the latter subject to means testing.

What is being done to promote delivery system integration and care coordination?

GPs are responsible for care coordination as part of their overall contract with the NHS. For instance, the 2018–2019 GP contract aims to improve care coordination for older patients by requiring practices to have a “named accountable GP” for all patients over age 75. GPs also have financial incentives to provide continuous monitoring of patients with the most common chronic conditions, such as diabetes and heart disease.

GPs work increasingly in multipartner practices that employ nurses and other clinical staff to carry out much of the routine monitoring of patients with long-term conditions. These practices also have some features of a medical home. For instance, they direct patients to specialists in hospitals or to community-based professionals, like dietitians and community nurses, and maintain treatment records of their patients.

The 2012 Health and Social Care Act charged NHS England and CCGs with promoting integrated care, which is defined as closer links between hospital- and community-based health services, including primary and social care.

In 2016, NHS organizations and local authorities were brought together in 44 sustainability and transformation partnerships with the aim of planning services together. Fourteen of these partnerships have become integrated care systems (ICSs), in which local authorities, GP networks, and local hospitals assume joint responsibility for sharing resources across their populations (1 million people on average).39 The formation of integrated care systems, which are modeled on accountable care organizations in the United States, is currently voluntary. The individual organizations in the systems are still legally accountable for their own budgets.

Knowledge on care integration was gained from 50 vanguard sites, smaller pilots of collaborative working groups, launched in 2014. These 50 sites delivered integrated services for older people or those with long-term conditions via scaled-up general practices and collaborations between hospitals and care homes. Evaluation of these vanguard programs has shown the potential to reduce hospital use among vulnerable populations through better community-based care. For example, a project to improve health care in care homes led to 23 percent fewer emergency admissions and 29 percent fewer accident and emergency department attendances than in other parts of the country.40

What is the status of electronic health records?

The NHS number assigned to every registered patient serves as a unique identifier. All general practice patient records are computerized. Since April 2015, all GP practices have been contractually obliged to offer patients the choice of booking appointments and ordering prescriptions online. As of March 31, 2016, practices are required to offer patients access to their own detailed coded record, including information about diagnoses, medications and treatments, immunizations, and test results. Practices are not required to allow patients access to information that clinicians enter in free-text fields. When electronic records are not available to patients, such as in dentistry, they can request a paper copy.

The NHS is aiming to move to a paperless system across primary, urgent, and emergency care services by 2020. Beginning in October 2018, all NHS providers are required to receive all referrals to outpatient services from GPs electronically.41

The NHS website serves as a single point of access for patients to register with a GP, book appointments and order prescriptions, access approved apps and digital tools, find information about local services, and learn about health in general. The website will eventually allow patients to speak to their doctor online or via video link and view their full health record.42

How are costs contained?

Costs in the NHS are constrained by a national health care budget that cannot be exceeded, rather than through patient cost-sharing or direct constraints on supply. NHS budgets are set at the national level, usually on a three-year cycle. CCGs are allocated funds by NHS England, which closely monitors their financial performance to prevent overspending. Both CCGs and NHS providers are expected to achieve a balanced budget each year.

Since 2010, the allocation of funds by the central government has grown much more slowly than the long-term historical rate, which averaged 4 percent in real terms between 1949–1950 and 2010–2011.43 Between 2010–2011 and 2014–2015, average real-term growth in spending on health rose by 1.2 percent and is projected to rise by 2.7 percent in real terms by 2019–2020.44

The mismatch between funding, demand, and the cost of providing services has led to NHS hospitals and other providers accumulating an underlying deficit of GBP 4.3 billion (USD 6.1 billion).45

Although some of the savings targets have been met in the past five years, the financial pressure on the NHS is being associated with some deterioration in the quality of care — notably waiting time targets.46

Cost-containment strategies to date include freezing staff pay increases, supporting the increased use of generic drugs, reducing DRG payments for hospital activity, managing demand, and reducing administration costs. In 2016, NHS Improvement launched a program to help hospital providers generate savings through more efficient use of staff, more cost-effective purchasing of drugs and medical equipment, and better management of estates and facilities. If implemented, the program could save GBP 5.0 billion (USD 7.1 billion) by 2020.47

There are a number of tools provided by the government-funded Rightcare program whereby local purchasers can maximize value by addressing unwarranted variations in utilization and clinical practice. Local purchasers can also run competitive tenders for certain services.

Costs for prescription (branded) drugs are contained through a voluntary agreement between the U.K. government and the pharmaceutical industry. The latest scheme, which came into force in January 2019, is known as the Voluntary Scheme for Branded Medicines Pricing and Access and will run for five years. It caps the growth in the sales of branded medicines at 2 percent per annum.48

This scheme runs parallel with the cost-effectiveness appraisals by the National Institute for Health and Care Excellence , which tends not to recommend new drugs as cost-effective if they exceed GBP 20,000– 30,000 (USD 28,500–42,675) per quality-adjusted life year. For drugs or treatments that have not been appraised by the Institute, the NHS Constitution states that CCGs shall make rational, evidence-based decisions.49,50

What major innovations and reforms have recently been introduced?

In October 2014, NHS bodies, led by NHS England, published the Five Year Forward View, which sets out the challenges facing the NHS and strategies to address them.51 These include pilot programs across England to test new models of care, among them:

- scaled-up multidisciplinary primary care

- enhanced health care in long-term care homes

- vertically integrated hospital and community care

- networks to improve emergency care.

Five-year strategies have also been published for improving cancer and mental health services, and better prevention, including a diabetes prevention initiative.52 The General Practice Forward View sets out strategies to reduce workforce shortages in primary care and to streamline GP workloads.53 These initiatives have recently been consolidated in the NHS Long Term Plan, published in early 2019. This 10-year plan sets out a vision for local integrated care systems to improve population health, new national strategies on cardiovascular and respiratory disease (in addition to cancer and mental health), and new primary care networks to better link together general practices.54

The authors would like to acknowledge Anthony Harrison, the author of earlier versions of this profile, as well as Sean Boyle of LSE, Claire Mundle and Sarah Gregory of the King's Fund, and Sandeepa Arora of the Nuffield Trust.